Surgepays update

It’s been a while since I discussed Surgepays (see here and here), and the recent Q3 results as well as my recent chat with the CEO are a good opportunity to provide an update about the company.

Last year was a relatively successful year for the company, where it was able to grow ACP subscribers from basically zero to more than 220k. This had a strong impact on revenues but relatively muted impact on earnings given the relatively large upfront customers acquisition costs. Much of this subscriber growth was achieved via the ‘circus-tent’ method (see previous write-ups), which are relatively expensive given the commissions (now called ‘marketing expenses’) paid out to field agents.

But 2023 is looking much different; top-line growth slowed down significantly, and earnings and cash generation expanded significantly. Like any commodity business with zero pricing power, the focus has to be on costs. And in order to reduce costs, Surgepays started to buy tablets in bulk - saving 20-30% per tablet, thereby drastically lowering customer acquisition costs - and shifted the ACP enrolment to the store channel. Besides lower acquisition costs, the latter is also supposed to strongly improve churn (a big cost amongst ACP participants) and provide cross-sell opportunities of other Surgepays products in the stores.

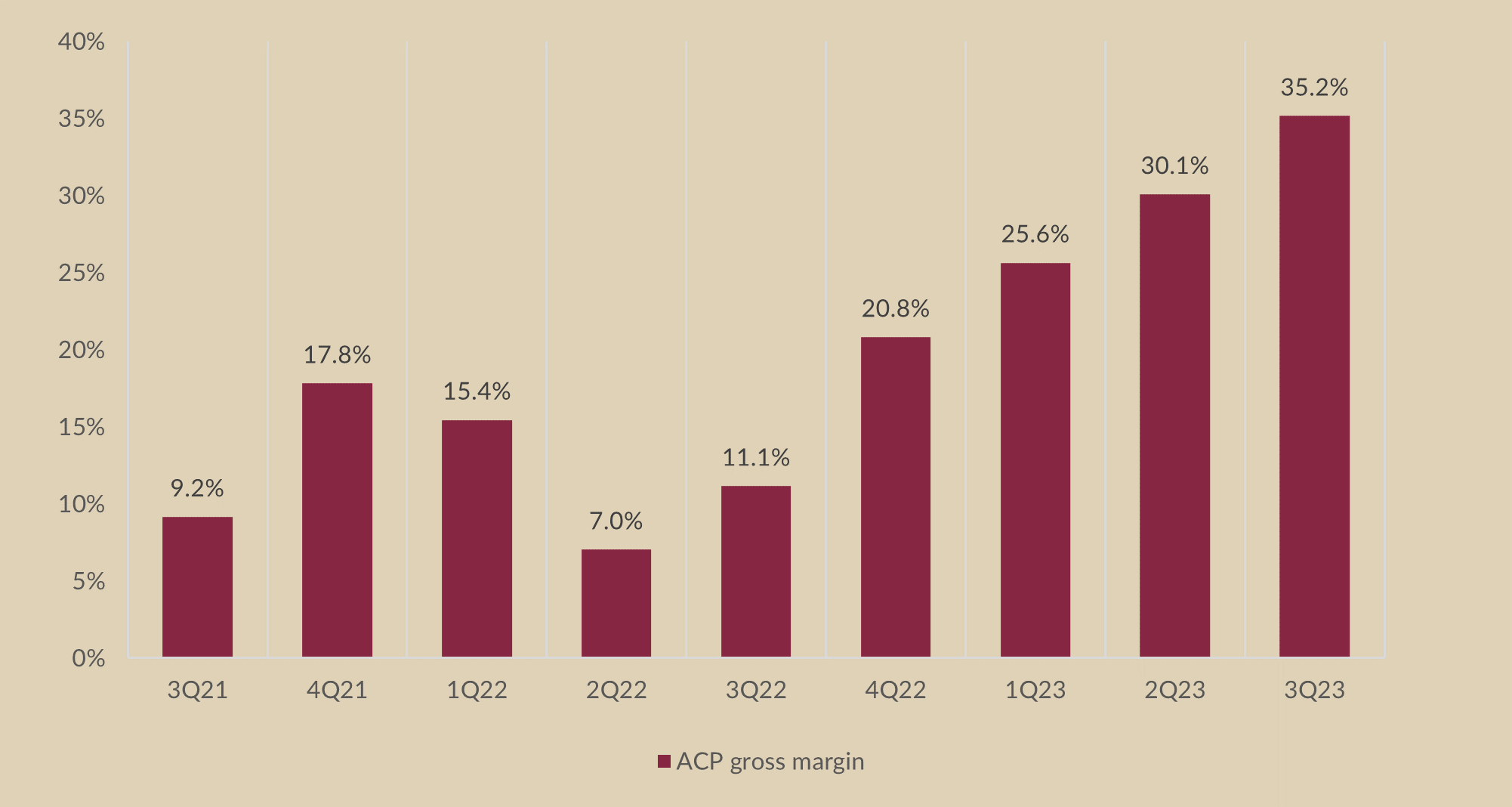

Fast forward ~one year, Surgepays has indeed successfully reduced acquisition costs, as can be seen in the ACP gross margin increasing to >30% in the latest quarter.

However, growth in new subscribers slowed down significantly. While many leads are generated in stores, new customers need to authorize Surgepays via text messages to handle their subscription. This is apparently a big hurdle, and the main cause for a relatively low conversion of the store leads.

Surgepays is trying to address this issue, providing the opportunity to sign up for the ACP via tablets on the counter in convenience stores. This is supposed to greatly facilitate sign ups by streamlining the process and removing the need for Surgepays to contact potential subscribers via text messages. The progress so far is encouraging. Surgepays is working towards 1,800 stores with this LCD interface on the counter, and is targetting to equip 6,000 stores over the next six months.

Given basically no growth from the ‘circus-tent’ model anymore, growth in ACP subscribers will continue to be relatively muted until Surgepays is able to make the store channel work.

But despite all this, the next few quarters are likely to be interesting for several reasons.

First of all, the biggest near-term value driver is the renewal of the ACP program, the funds of which are expected to be depleted by Q1 24. In order to avoid massive (political) damage, the ACP will have to be renewed, sooner rather than later. The ACP has to be renewed before 2024. As the ‘deadline’ of running out of funds approaches, broadband providers will have to notify recipients and ramp down the service. That’ll take time, and ISPs will not wait until funds are depleted.

Pressure on congress is increasing and I expect some news over the next months, given the most recent request by the administration for $6bn funding. This will be enough for FY24, but the funding issue need to be addressed again in six months’ time.

Nonetheless, Surgepays is positive the program will be renewed, particularly given the consequences. Failure to refund the ACP will be disastrous, in many ways. There are now >20m households on the program, and increasing daily. Imagine the damage (of all sorts) of cutting these people of. Also, the ACP provides information that is critical to the implementation of the massive $42bn BEAD program, which will become much more inefficient should ACP disappear.

And while itself being a drop in the budget, there are many ways to fund the ACP. Federal broadband subsidy programs chaotic, and many overlap. Programs like BEAD and ACP are considered much more efficient and important and actually make other broadband programs redundant. Programs like High-Cost, Lifeline and Reconnect could easily be discontinued, and the funding used to make ACP sustainable.

Furthermore, Q3 was an interesting quarter as we saw the first ‘true’ cash flow generation ability of Surgepays under the ACP program. We know that growth and cash flow are very much communicating vessels, and much growth is financed via working capital (and the instalment sale financing).

Given roughly flat growth in Q3, this was reflected in the company’s working capital needs (i.c. no material investments), and Surgepays generated about $9m cash to the firm. In other words, as growth slowed cash flow generation surged given little need to pay for (new) growth.

This has strong implications for next year. Assuming 280k ACP subs by FY23, roughly 5k net new subs per month (i.c. roughly the average growth in this year) based on an unchanged c.8% monthly churn, Surgepays could generate c. $35m ebitda in 2024 – assuming this continued slow growth pace. But free cash flow conversion would be very high, almost 100%. Assuming 85% conversion would result in $30m free cash flow.

Given the current Q3 balance and assuming similar cash generation in Q4, this would result in a $40-50m net cash position by FY24, or roughly 40-50% of the current market cap.

Surgepays intends to use its generated cash actively.

One important use of the cash flow will be to fund the upcoming launch of Surgepays’ own wireless mobile product, LinkUp Mobile. I’m still assessing the potential, but I understand that this product could generate similar margins as the current ACP revenues. This new development is promising given the company’s existing ACP subscriber base and related household data. Surgepays intends to leverage this existing base and quickly grow its offering. The product will be marketed along with the ACP on the LCD screens on store counters.

Another important development will be acquisitions, where Surgepays intends to acquire non-ACP wireless companies with the potenital to leverage its platform and enhance cross-selling opportunities.

The main point is that even though ACP subscriber growth has slowed (actually, because it has slowed), Surgepays is very focussed on leveraging its current cash flow generation and diversify its revenue generation away from the ACP. I believe this is a smart more, which would much increase visibility in earnings generation and benefit the company’s valuation.

So far I’ve always treated Surgepays like an option. While very cheap based on the company’s realized growth, I believed that the large dependence on (and uncertainty of) the ACP program and related regulatory framework, and perhaps areguably chequered past of the CEO would act as a drag on the company’s valuation. That more or less seems to have been the case so far. But while there’s always the risk that something might come out of left field with this company, I appreciate that even assuming muted growth for the ACP program, Surgepays is now focussing on diversifing away from the ACP and provide for new growth avenues.

In a few quarters, I’m expecting Surgepays to have several thousands of stores equipped with its ‘marketing tablets’, accelerating ACP subscriber growth, and >100k subscribers on its new mobile wireless product. I’ll be assessing the company’s performance based on these targets.

Thank you for reading. If you enjoy this service, please ‘like’ and hit the “share” button below.

Hey ToffCap,

Any thoughts on trading the possible ACP renewal? 227 cosponsors (up 2 since yesterday) both Democrats and Republicans. Last price for the Aug calls @ 5 for $0.37, or @ 2.5 for $1.35.

https://www.congress.gov/bill/118th-congress/house-bill/6929

Once bitten, twice shy. A lesson in doing my DD on the CEO properly for me. Too many contingent factors for this to be anything other than an 'option' (and hence very small) trade