SurgePays

This write-up is based on my recent tweets on the company and includes some updated thoughts and figures.

Surgepays offers telecom, mobile broadband and various fintech services to underbanked and underserved communities. Keeping it simple, the company offers two different products. The ‘oldest’ product is a software platform, installed in ~8,000 local stores / bodegas, that enables the owner to offer various basic financial services, such as activating / topping-up prepaid wireless accounts, take payments for prepaid wireless customers, reload debit cards, gift cards, etc. The second and more recent offering is providing mobile broadband services under the relatively new Affordable Connectivity Program (ACP). Under the ACP – a now permanent, $14bn program which began in 2021 and is the successor of the Emergency Broadband Benefit program – Surgepays provides free internet to low-income households. The ACP is a consequence of the covid lockdowns; as people were confined at home, many experienced problems working from home or following school as they had no internet. The market is very large, with an estimated 30m-60m households eligible for the program, and more than 13m households have signed up for the ACP so far.

Of the two offerings, the mobile broadband services is the most exciting given its rapid growth. It will also be the biggest contributor to earnings over the next few years. This write-up focusses only on this segment.

Surgepays, as a MVNO, is licensed to provide its services under the ACP in all 50 states. The company sets up tents in high-footfall locations and/or in the neighbourhood of the local shops on their network and signs up as many people as possible. The offering is a free sim-card (with free internet) and a tablet at a cost of $11. Customers can use the sim-card with the tablet or use it in another device.

The offering has attractive unit economics. The costs for Surgepays are $80-$90 for the tablet, ca. $45 commission for the salespeople and a recurring $15 per month per subscriber. The government then reimburses Surgepays $100 for each tablet and $30 per month per subscriber (as long as the subscriber has actually been using the free internet). Reimbursement generally occurs after 30-60 days. Surgepays has the good habit to regularly update the market of the numbers of subscribers they currently have; as of October 5th, the company has over 220,000 subs (the target for 2022 was 200,000).

With these numbers we can now make a simple model to see what this all means for the future earnings potential of the company. Please keep in mind that all calculations / estimates are back of the envelope, which is good enough to get an idea of what’s going on.

But let me first take a step back. When I was reading up on Surgepays, I got excited about its potential but was surprised of the company’s guidance for 2022 ($15m ebitda) and analyst estimates for 2023 ($35m ebitda). My initial reaction was ‘no way’. No way they’d hit $15m ebitda in 2022 and no way 2023 ebitda will be only $35m if this level of growth continues. The back of the envelope reasoning is simple; for 2022, the ratio of new subs / existing subs will be sky-high and as such also customer acquisition costs (cost of tablet + commissions). Costs are front-loaded, and it takes 30-60 days to be reimbursed by the government. By the time you are reimbursed, additional subs should be signed. As such, 2022 will see a lot of front-loaded costs and a relatively low average subscriber case contributing to revenues. In contrast, 2023 will have way better economics given a much higher existing subscriber base generating recurring revenue right from the start. 2023 is where the fun should start.

Every month Surgepays signs on new subs and provides them with a tablet and a free internet subscription. The pace of new subs has been 1,000-1,500 new subs per day over the past six months. However, this is not ~1,250 * 30 = 37.5k new subs per month; it’s 1,000-1,500 per day as long as they have devices. New subs are added based on how many devices Surgepays was able to purchase a priori. So if they run out of devices 20 days into the month, they stop signing on new subs for the rest of the month.

But if demand is apparently not a problem, why this strategy? That’s mainly the consequence of the way the company has chosen to finance its growth. Keeping it simple, an average micro-cap would just have raised a bunch of equity and bought devices en masse, but that would have meant a lot of equity; think 275k subs * $85 per device = $23m(!) - and that’s just the devices, so excluding commissions etc. Sure, growth would have been more rapid, but the dilution would have been massive. Conventional debt was also difficult; who would lend $23m to a micro-cap with negative ebitda? There are of course a myriad ways of financing, but you get the point.

Surgepays chose a more conservative (and slower) growth path by using factoring, which is basically borrowing against your receivables. It’s a form of short-term debt generally used by companies that have good visibility on receivables and need short-term cash. Dependent on the quality of receivables (which in Surgepays’ case is very high, given that payment is coming from the government), companies can generally borrow up to ~80% of receivables with short duration. Surgepays did exactly that and borrowed ~$6m at a mid-20% interest rate. Now that may seem high, but it’s actually a pretty low rate for receivables financing. I’ve seen plenty of cases of factoring with 1-2% weekly rates.

Now this type of financing creates an interesting dynamic, as revenue growth depends on the growth of receivables. So the more subs the company adds, the higher the receivables, the more devices it can purchase up front and thus the higher the revenue growth, and so on. This is what the company means when referring to growth that should be accelerating as the company grows. We will know more in the coming month as the company reports, but at a recent conference the CEO mentioned being close to signing a new funding agreement; off the factoring and onto more flexible, cheaper program, based on receivables and inventory (which should now roughly be $12m-$15m). This instrument should be up to $50m in size, which would allow Surgepays not only to buy more devices (and thus accelerate growth), but also to lower the cost per tablet by providing the manufacturer a down payment on new devices. According to management, the supply of tablets should not be a problem.

Now let’s look at some rough, back-of-the-envelope numbers. I’ve assumed 23k net new subs for the remainder of 2022, 2023 and 2024 and $135 acquisition costs (device + commission) + $15/sub data usage. I believe these are conservative assumptions, as they’ve grown roughly 21k new subs per month over the past 6 months (so no acceleration assumed) and the cost of tablet should come down as the new financing is in place.

As can be seen, 2022 is the year of the ramp up:

And 2023 is where earnings really start to ramp:

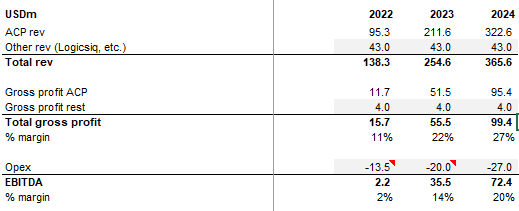

Dragging the assumptions to 2024, we get the following estimates:

I have made some simplistic assumptions regarding the rest of the business (i.c. no improvement). I’ve also been relatively aggressive on my assumptions of operational expenses.

Note that 2022 is clearly a revenue story, not an earnings story. $15m ebitda for this year was always a stretch, particularly as the company is expensing its acquisition costs instead of amortising them over a longer period (the $15m ebitda guidance was based on amortisation of acquisition costs, which the company didn’t do). That said, whether they’ll hit their ebitda target or not this year (they won’t) has never been really important to me, as that’s peanuts compared to what Surgepays could be earning as of next year. That’s where the real earnings will start. I believe my estimates are conservative; put the numbers in that you think are reasonable for the growth and the cost of subscribers, but it’s not a stretch to think of >$40m ebitda in 2023 and almost double that in 2024. What multiple would you put on $40m 2023 ebitda growing ~100%?

Let’s now look at recent results, which caused a bit of confusion in the market. Comparing 1Q and 2Q estimates with the actuals we notice a couple of things. First, realised revenue is very impressive. We also notice ACP gross profits (Surge Phone + Torch Wireless) drop from $2.2m to $1.4 despite clearly higher revenues; this has scared the market a bit. There are some reasons for that. One is that some opex has been reclassified as cogs. Another reason is that Surgepays has to pay $2-3 per new Torch Wireless sub (this is part of the deal following the acquisition of Torch, which allowed Surgepays to expand its services to all 50 states), but that’s small as Torch subs are ~70k. A third reason, which was alluded to in the call, is that cost of devices has crept up quite a bit, easily $10-$15 per device. This alone has quite some impact ($0.5-0.9m). As mentioned, Surgepays soon intends to move away from just-in-time buying, which is something they can do with the new financing. This will save $15-$20 per device.

Another important reason is attrition. As recently mentioned by the CEO, ca. 40k new subs have apparently been using their new tablet on wifi as these users did not understand that internet was actually free. Surgepays does not receive reimbursement ($30 for the $15 cost of data usage) if users do not use the sim-card they received from the company. Surgepays is working to address the issue, sending reminders to new subs that they can use the sim-card with free internet on another device. This is an important metric to keep assessed, though the company does not provide numbers on the actual attrition. I have included what I believe are very aggressive assumptions (6%-7% monthly) to be on the conservative side and to show that even at high levels of attrition, the company should be able to finance its growth and grow earnings at a strong pace.

To keep in mind: If a sub stops using the service (ie does not use the sim-card with free internet), he/she is kicked out of the program (end-of-month check) and Surgepays will only be ‘on the hook’ for the part of the month where the sub actually used data. However, Surgepays is nonetheless entitled to a full $30 compensation even if the new sub signed on mid-month. I’ve assumed the net effect to be nil.

But I believe at this point we should be careful not to complicate things. Surgepays is just starting to ramp up big time, and it’s way early in the process. In my experience, there are always more costs than previously expected in a ramp up story, and there’s also always room for improvement. I do not believe everything will go smoothly; mistakes will be made and these guys will learn (hopefully). 2Q was a very small quarter compared to what will come. Let’s also keep in mind that this is still a tiny micro-cap company. That said, again keep in mind that Surgepays will probably miss their $15m ebitda target for this year.

Finally, let’s look at the valuation. Again, what multiple would you put on $35m ebitda in 2023, knowing you’ll have a good visibility on doubling ebitda in 2024 (remember how important the existing sub base is at the beginning of the year). Let’s say 7.5x in the current market and given the company’s size; that gives us ~$260m enterprise value. Without complicating stuff, I’ll assume zero net debt (the company has 5.3m warrants outstanding at an exercise price of $4.73, good for $25m) and 17.4m fully diluted shares outstanding (the CEO owns ~30%). That gives us roughly a $15 share price in 2023, compared to $5.5 today. If interested, one could also play the warrants for more leverage.

One last side note. Surgepays is working to spin-off a division called LogicsIQ. This segment should be good for ca. $20m revenue and a few million ebitda. I understand from the CEO that all the paperwork has been completed and filed; we should get more info at the next quarterly results.

As always, do your own diligence.

For more content, follow me on Twitter.