ToffCap's Monday Monitor #10

Interesting companies and event-driven trades

")

ToffCap’s Monday Monitor provides a snapshot of interesting potential investments and event-driven trades we find while turning over many rocks, with a special focus on companies that screen cheaply and catalyst trades. The list is dynamic; it continues to grow and change. If you have interesting additions to the list, feel free to contact us at contact@toffcap.com or on Twitter.

Enjoy!

Disclaimer. ToffCap’s Monday Monitor is provided for informative purposes only. No due diligence has (yet) been performed on the names on this list. The list might change strongly on a regular basis. This overview does not constitute advice; always do your own due diligence.

Overview

I. Company watchlist

II. Catalyst trades

I. COMPANY WATCHLIST

Annotations for a selection of interesting companies with seemingly strong upside potential.

Additions this week:

ADF Group and Daktronics. We have a recent update on two of our favorite companies, who remain stubbornly cheap despite strong earnings growth (ahead).

InPost (INPST Netherlands – PNL 26bn). Polish operator of Automated Parcel Machine lockers (trading in Amsterdam). Unique proposition; high-growth company in a generally very sleepy market. InPost continues to perform well and take market share from legacy postal players. Already dominating the Polish market, which is rapidly becoming a cash cow, and is currently focusing on growing in France and the UK. The latter has now uncapped capacity given the acquisition of Menzies Distribution. Reasonably cheap given growth profile (though watch for IFRS 16) and long-term ‘disruptor’ potential.

Talen Energy (TLNE US – $ 3.2bn). We’re once again highlighting Talen Energy (up c. 20% since our highlight as an event-driven trade). Talen is a power generator and infrastructure company, mostly nuclear related. The company recently exited bankruptcy and has been trading OTC. Could be an interesting set-up given the recent request to uplist to a major exchange as well as the strongly increased interest in nuclear power generation. Classic pre-coverage period.

Bel Fuse (BELFB US – $ 585m). Bel Fuse manufactures and designs electronic components (e.g. integrated connectors modules, cable assemblies, aviation spares, powerline products, etc.). Interesting business given relatively sticky customers and strong end markets. Ebitda could double by 2025 given market tailwinds, as well as restructuring efforts. Trading at just ~6x 2022e ev/ebitda vs. peers 13-18x. H/t @InvestSpecial for the highlight and @AtaiCapital for the original pitch.

SFC Energy (F3C Germany – € 380m). SFC Energy develops, produces and markets fuel cells for e.g. electric vehicles, remote industrial applications and mobile and stationary defense applications. Interesting high-growth and profitable play on recurring sustainability theme. Order backlog growing nicely (roughly 40% yoy). Near term cost headwinds due to India factory ramp up. Might need to raise cash given limited free cash flow generation. Market cap + liquidity reaching interesting thresholds.

eDreams Odigeo (EDR Spain – € 830m). We highlight Andrew Walker’s excellent podcast on eDreams. eDreams is one of Europe’s largest OTA, currently transitioning from a transactional to a subscription business model with its PRIME loyalty program. This should lead to higher margins, visibility and resilience. Key metrics continue to improve. The shares are cheap due to skepticism of the model change + the company using non-standard financials metrics. Could 2-4x in a few years if the transition is successful and market valuation shifts (more) towards recurring revenue comps.

Previous additions (excl. companies no longer on the watchlist):

Not edited since initial inclusion.

Civitanavi (CNS Italy – € 113m). Civitanavi designs and develops technology solutions of inertial navigation, geo reference and stabilization systems for both industrial and defense use. CNS IPOed in 2022, but got wrecked after reducing its 2023 guidance. The sell-off could provide an interesting entry point into a profitable company with a strong balance sheet (~26% of EV in net cash), good market and product positioning and what looks like solid growth ahead. @BerkelKip has a recent tweet on CNS.

Aplisens (APN Poland – PLN 252m). Aplisens manufactures process instrumentation (differential pressure transmitters, hydrostatic level probes, level transmitters, valves, digital indicators, gauges, etc.). Aplisens’ growth appears to have been inflecting positively over the past few years. The company recently published H1 23 results, showing ~22% revenue growth yoy and ~PLN 17m income; assuming H2 = H1 for simplicity, Aplisens is trading at roughly 7.5x 2023e p/e for >50% yoy growth in H1. Good cash flow generation and roughly 3.5% dividend, if you’re into this. No sell-side coverage.

Twin Vee PowerCats (VEEE US – $ 17m) and Forza X1 (FRZA US – $ 14m). We’re keeping an eye again on these two power boat manufacturers for the first time since the spin. Both micro-caps back net cash balance sheets (closed to zero EV), and Twin Vee still holding ~44% of Forza. Both companies now seem to have some interesting catalysts ahead that could bring the valuations back to a more sensible level: Twin’s acquisition of AquaSport, now back to production, and Forza’s ramp up in deliveries. Check the comment section of this old VIC write-up for some info and CarlosM’s more recent work.

Barco (BAR Belgium – € 1.8bn). We highlight the recent write-up. High-quality compounder. Belgian technology company with main focus on visualization technologies. Three separate divisions (i.c. no synergies) with continued strong growth potential given secular tailwinds). Continued strong qoq improvements. Barco trades at ~10x 2023e ev/ebitda for >15% ebitda growth over foreseeable future. Shares down YTD despite strong performance due to uncertainty surrounding the health of co-CEO (and major shareholder) Charles Beauduin, though shouldn’t impact the business.

Daktronics (DAKT US – $ 358m). Daktronics is a manufacturer of electronic scoreboards and large screen displays for sporting, commercial and transportation applications. The company has a strong market positioning and is a well-respected player. In some ways it reminds us of Barco, which also has a large screen division (though operates in other markets). Daktronics suffered during covid, but supply chain challenges have now eased and the pricing environment has improved. Fundamentals are improving, with growth returning, margins improving and NWC normalising. DAKT is positioned for further growth, which the company expects to realise over the next quarters. Q4 (ending April 2023) was very good, which bodes well for the seasonally strong H1. Daktronics is trading at <4x ev/ebitda on our 2023 estimates of earnings and cash flow generation; continued progress should at least double this multiple, on higher earnings. Surprisingly, there’s no coverage on this company (yet). H/t AltaFoxCapital for this idea.

ADF Group (DRX Canada - CAD 115m). A ToffCap favorite. We reiterate our stance, as recently tweeted. ADF’s Q1 results were extremely strong, but have not (yet) shown the full extent of the company’s recent efficiency improvements. Going forward, ADF will double the amount of steel passing through the automation platform. This, combined with relatively more higher value-add projects on its record order backlog and a good amount of operating leverage, could lead to $40-50m ebitda in FY24 (current year). Stock could 2-3x over next ~18 months. Write-up here.

Oil tanker basket (think TNP, STNG, EURN, TORM, HAFNIA, FRO). We’ve brought back some crude and product tanker stocks on our watchlist . Rates have been holding unusually well in what is normally a weak quarter. This bodes well for the high season. Fair warning, careful with tanker stocks; a short overview of the potential explosivity of tankers (both up and down).

Hudson Global (HSON US – $ 61m). Hudson is a Recruitment Processing Outsourcer. Left for dead after several headwinds. Revenues are generally highly recurring in this business, creating visibility. Margins could be at the trough now that Coit acquisition mess appears to be under control. Ebitda could grow >30% pa over next few years (off low base). Trading at ~3x 2023e ev/ebitda, with $ 20m net cash on balance sheet and > $ 300m NOLs available. FCF conversion ~100% given asset light business and NOL usage.

Brunswick (BC US – $ 5.4bn). Cool boats (and parts). Outboard engines continue to gain market share, and Brunswick is profiting from this trend. Vertically integrated. Duopoly with Yamaha. 7-8x p/e despite industry headwinds, strong ROICs. Many thanks to Roojoo for this idea.

II. CATALYST TRADES

Event-driven.

The list is getting longer and longer. We are changing the format in order to make it more accessible; we hope you’ll find it useful. Should you have any comments, just let us know.

New additions and updates

Vista Outdoor (VSTA US). Will spin its outdoor segment. Recently filed a Form-10, intention to spin in Q4. Could be interesting given underlying free cash flow generation + ‘anti’-ESG character of part of the assets.

SharkNinja (SN US). Recent weird spinoff. Could have quite the earnings power; peers trade at much higher multiples. Classic pre-coverage period. See Andrew Walker for recent write-ups.

Kellogg (K US). Approved the spin of WK Kellogg (KLG). Kellogg will be renamed Kellanova. Separation to become effective on October 2. Record on 9/21; 1 KLG share for every 4 K shares of K.

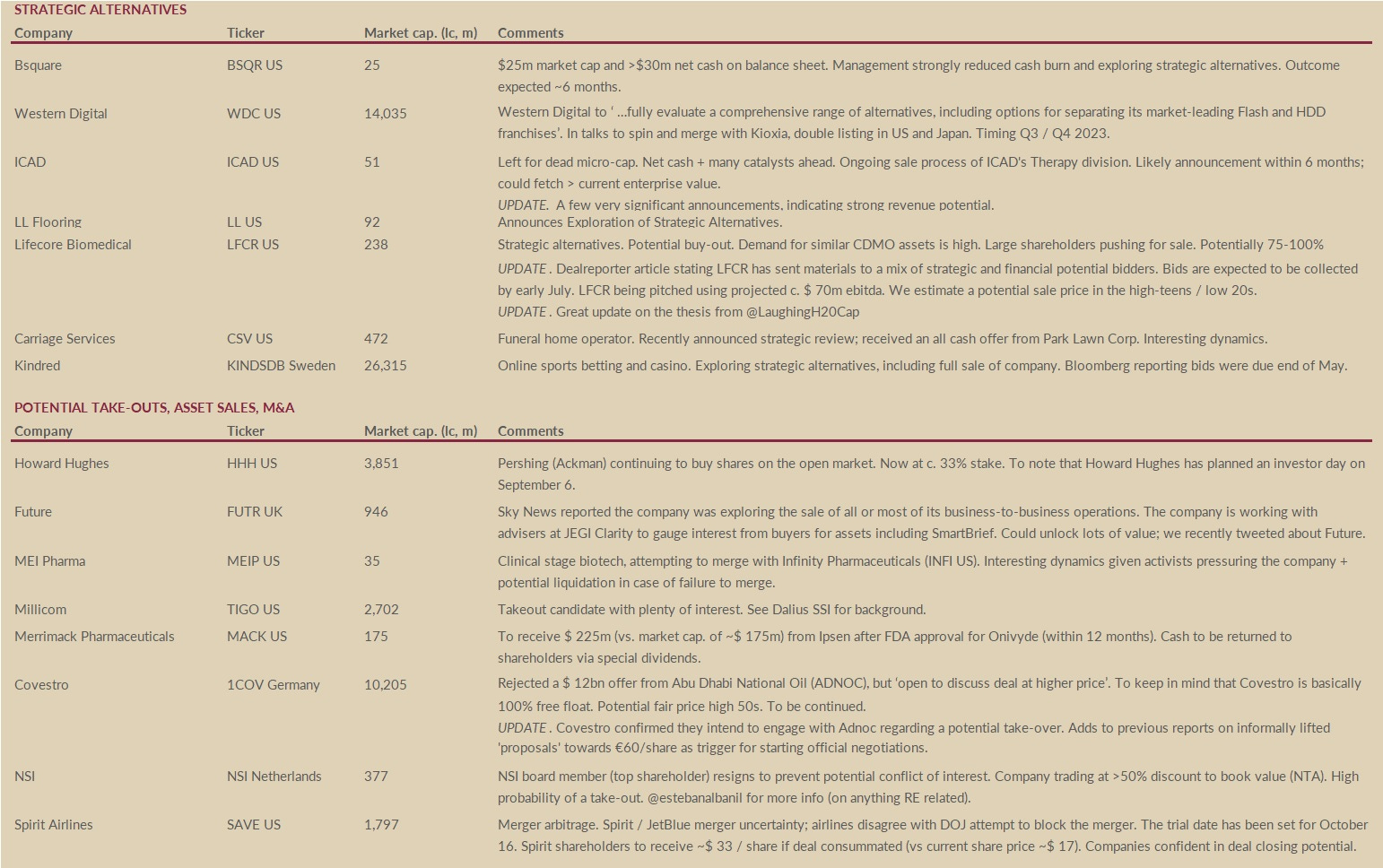

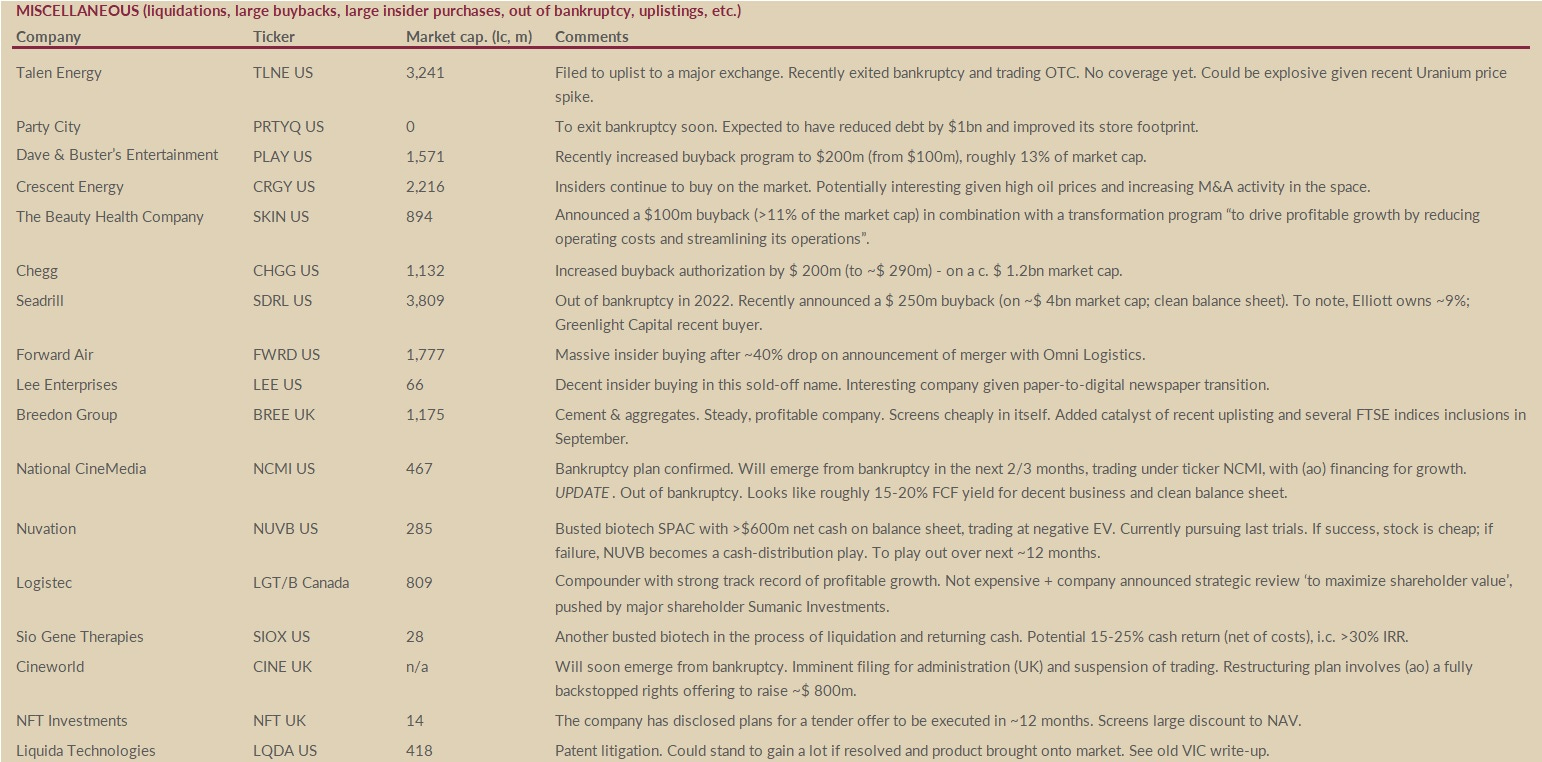

Talen Energy (TLNE US). Filed to uplist to a major exchange. Recently exited bankruptcy and trading OTC. No coverage yet. Could be explosive given recent Uranium price spike.

Party City (PRTYQ US). To exit bankruptcy soon. Expected to have reduced debt by $1bn and improved its store footprint.

Dave & Buster’s Entertainment (PLAY US). Recently increased buyback program to $200m (from $100m), roughly 13% of market cap.

Crescent Energy (CRGY US). Insiders continue to buy on the market. Potentially interesting given high oil prices and increasing M&A activity in the space.

The Beauty Health Company (SKIN US). Announced a $100m buyback (>11% of the market cap) in combination with a transformation program “to drive profitable growth by reducing operating costs and streamlining its operations”.

BSquare (BSQR US). $25m market cap and >$30m net cash on balance sheet. Management strongly reduced cash burn and exploring strategic alternatives. Outcome expected ~6 months.

Calumet (CLMT US). Calumet is preparing to spin its MR unit in a few months, targeting > CLMT's current EV. Management recently dedicated a slide to what they believe is an intrinsic value range for Calumet’s equity: $31-56 p/s (vs ~$19 today).

NCR Corp (NCR US). Spin-off of ATM-related business in Oct. 2023. Potential large SOTP value unlock.

UPDATE. NCR held investor days for stubco and spinco (Voyix and Atleos). Slide decks to be found online. Spin on track.Aramark (ARMK US). Will spin its uniform business (Aramark Uniform Services). The remaining company will focus on Food & Facilities Services. Form-10 recently filed. Spin-off planned before year-end.

UPDATE. Will spin Vestis (VSTS US) on September 30 (distribution date). Management expects 5-7% organic growth and 4-6% EBITDA margins expansion over 5 years.LICT (LICT US). Changed distribution date for its MachTen (MACT US) spin-off to August 31 (from August 14). Shareholders to receive 150 shares of MachTen for every 1 share of LICT. Could have some interesting dynamics given small spinco size.

UPDATE. Michigan subsidiary MachTen $MACT now listed; +19% since listing.Telekom Austria (TKA Austria). Telekom Austria (controlled by America Movil) to spin-off the cell tower, renamed EuroTeleSites AG, in ‘autumn 2023’. For every four Telekom Austria shares, the shareholders will receive one EuroTeleSites share.

UPDATE. Tower unit to be listed in Vienna on September 22.Cia Brasileira de Distribuicao (CBD US). Spin-off with remainco trading at negative value. Great write-up from Clark Square Capital.

UPDATE. Spin completed. Exito and CBD stub still screening cheaply. CSC update here.

UPDATE. Little demand for Exito (EXTO US - CBD spin) post spin; might be interesting to keep an eye out on weakness.Covestro (1COV Germany). Rejected a $ 12bn offer from Abu Dhabi National Oil (ADNOC), but ‘open to discuss deal at higher price’. To keep in mind that Covestro is basically 100% free float. Potential fair price high 50s. To be continued.

UPDATE. Covestro confirmed they intend to engage with ADNOCregarding a potential take-over. Adds to previous reports on informally lifted 'proposals' towards €60/share as trigger for starting official negotiations.

Overview of event-driven trades

SPIN-OFFS (and related)

STRATEGIC ALTERNATIVES & POTENTIAL TAKE-OUTS, ASSET SALES, M&A

MISCELLANEOUS (liquidations, large buybacks, significant insider purchases, out of bankruptcy, uplistings, etc.)

Hi Toff,

Appreciate this -

For the misc list, you should add:

Yellow Corp $YELLQ - Good summary on the situation here https://twitter.com/DetiEth/status/1694272782106775701

This is very helpful!! Great post!!