A few micro-caps I'm looking at

IZEA, Butler National and Unifiedpost

A quick note. Going forward, we’ll be publishing write-ups more separately instead of lumping them together as we have done recently. This will improve the timeliness of the ideas and the readability of the posts.

IZEA Worldwide (IZEA US - $42m market cap)

IZEA Worldwide is a company that seems on the verge of a serious inflection. And I like to keep a very close eye on potential inflections.

IZEA is a company that focuses on influencer marketing and content creation. Pretty much most of their revenues are earned from Managed Services. This is when someone (typically a brand, agency or partner) pays them to provide custom content, influencer marketing, amplification or other campaign management services. They basically connect brands with influential content creators across various social media platforms to help companies promote their products and services.

Then there’s also some revenue from fees charged to software customers on their marketplace spend within the company’s platforms (Marketplace Spend Fees), a bit of license revenue and some other stuff.

But by far most revenue is generated within Managed Services, the segment that handles influenced marketing campaigns and content creation from start to finish.

Up until 2021 IZEA has been chugging along, growing revenues at a pretty slow pace and financing losses by issuing shares and using proceeds from short-term investments. Nothing special.

This sluggish growth path completely changed in 2021 and 2022 on the back of covid induced tailwinds. At the same time that the company introduced new platforms like IZEA Flex and expanded operations abroad, the market of influencer marketing took off like crazy. Demand for IZEA’s services skyrocketed, along with its revenues.

Though while the market remained pretty healthy, mainly given the still nascent market of influencer marketing, 2023 was a tough year for IZEA. The company lost a major non-recurring customer within Managed Services which significantly impacted revenues. At roughly the same time the company transitioned away from its legacy IZEAx and Shake platforms within its SaaS Services segments to newer platforms Flex and The Creator Marketplace, which caused some churn.

The loss was a wakeup call for the company, which increased its efforts to diversify its customer base. Meanwhile the shift to new platforms promises better pricing, lower churn and lower CACs, although revenues from these platforms remain relatively small.

Importantly, in H2 24 IZEA welcomed a new CEO, Patrick Venetucci, who replaced founder Ted Murphy. This is a good development; keep in mind that IZEA has yet to deliver its first year with positive operating losses.

It’s still too early to judge his progress, but I appreciate the new CEO’s action so far. He revamped the Board and increased focus on profitable growth. And over the past few months IZEA signed several interesting large customers such as Danone, Nestle and Coursera (though details are not provided).

Without making the story unnecessary long, the bottom line is that IZEA seems to have found new elan.

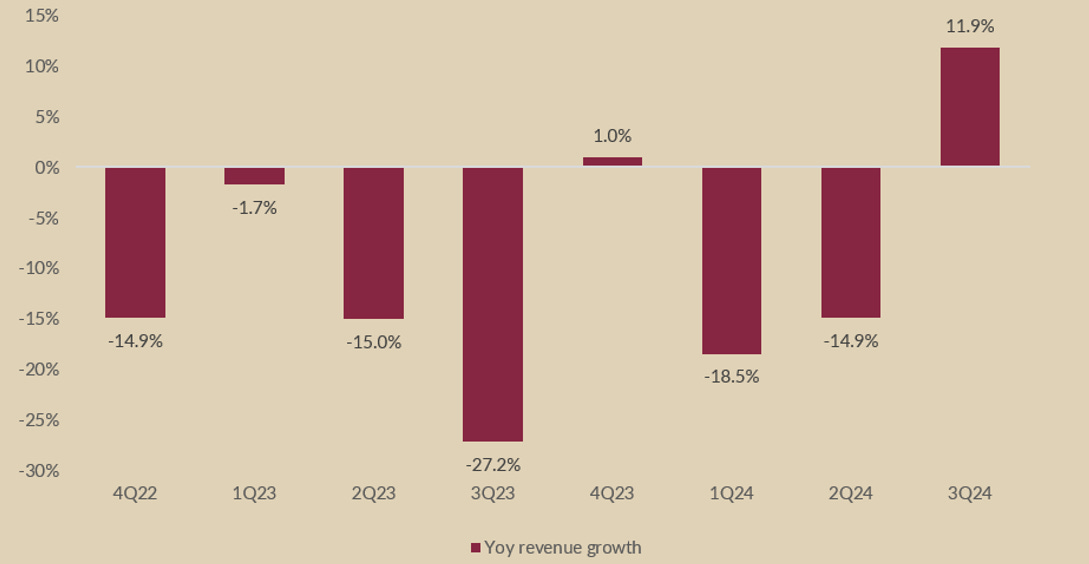

But importantly, this also seems to be reflected in the numbers. Look at the development of the yoy growth in Managed Services bookings over the past ten quarters…

… which pushed yoy group revenue growth finally into serious territory for the first time in two years.

The growth is even more interesting given that Q3 still experienced the impact of the loss of the large customer. Excluding revenues from this client, the adjusted yoy revenue growth would have been +27%. IZEA guided for continued yoy growth over Q4 24.

Overall, it seems that 2024 has been a transitional year for the company, with what appears successful efforts to fill the revenue gap left by the loss of the a large customer with more (profitable) clients.

Even more, IZEA has some big plans for the future. The company is targeting $76m in annual revenue by 2026, with ‘meaningful ebitda improvements in 2025’ and positive ebitda in H2 2026. This would mark significant revenue growth, roughly 50% p.a. over the next two years.

Nonetheless, while this all looks interesting there are a few things to keep in mind.

The new CEO did not reiterate the $76m target mentioned last by old CEO Ted Murphy in the Q2 24 call. He did speak about its 2025 business plan that will soon be unveiled. Of course that doesn’t mean that these targets are off the table, but perhaps the new CEO has a few different plans.

It’s also important to understand that despite all the recent progress, IZEA operates in a very competitive market. Innovation is key and the company will have to continue invest to stay competitive.

Lastly, it appears that we’re still be facing another year of operating losses in 2025.

But I remain interested nonetheless, and or a few very good reasons.

The first one is the progress described above. IF IZEA is indeed able to return to consistent topline growth, the company screens very attractively looking out a few years…

… but even more so given the significant net cash balance - $54m net cash on a $42m market cap.

So here we have a negative EV micro-cap, which seems to have found its way back to growth and is (finally) talking about reaching operating profitability.

Also, IZEA finally started to deploy this massive cash balance. They initially announced a $5m buyback not so long ago and more recently increased it to $10m, roughly 25% of the current market cap. Not bad.

One last interesting nugget. To note that GP Investments acquired a ~18% stake in the open market less than a year ago, at average prices quite higher than today.

Butler National (BUKS US - $115m market cap)

I’ll be shorter on this one, as it shouldn’t be a difficult thesis.

Butler provides aircraft modification, maintenance, repair and overhaul as well as gaming management services. The company operates two segments, Aerospace Products and Professional Services. Both are roughly evenly split in revenue generation.

The Aerospace segment focuses on aircraft modifications, avionics and regulatory-driven solutions. Think design, engineering, manufacturing, installation and repair of aircraft products and systems, both for commercial and military markets. Services range from special mission modifications to avionics upgrades and FAA-compliant installations.

The Professional Services provides management services in the gaming industry, including casino operations, through Butler National Service Corporation. It also offers architectural, engineering and management support services.

End markets have been pretty strong in both segments, and the company has done a good job in harvesting these tailwinds along with expanding its operations. As a results, Butler showed some good earnings, and the share price moved up strongly.

But despite the shares returning already +120% over the past year, Butler hits a few key items that make it still interesting to assess.

First of all, the stock popped up in our systems as insiders, in particular Joseph Daly (Director) - continue to scoop up shares despite the share price hitting new highs. This is one of the things we like to see when looking at insider transactions.

Also, the combo of what I believe could be stronger for longer end-markets, driven by enhanced investments in the defense sector as well as continued secular growth in sports wagering, should further drive demand for Butler’s products and services. This, combined with new product development, some targeted operational efficiencies and increased marketing efforts should be a driver for continued earnings growth over the next quarters.

The progress is also clearly visible in the company’s order backlog (mostly relating to Aerospace Products), which has moved to record levels. (Q2 25 ending Oct. 2024.)

Combined with what the company expects will be continued growth of the Professional Services segment – in part due to a contract with DraftKings to provide mobile and interactive sports wagering – this bodes well for the next few quarters’ earnings, particularly as the company will come up on easier comps (mainly Q4 25, ic the quarter ending April 2025).

Lastly, Butler mentioned that a top priority of the company’s cash management targets (as it expects to continue to generate healthy cash flow in the near term) will be to reduce the number of shares outstanding (i.c. buybacks).

All this makes it an interesting case.

As always there are some things to watch out for. At Butler I’m getting the feeling that now that some good times are rolling and the share price is moving strongly, insiders are starting to compensate themselves a bit too well. One example is a board member being granted 300k shares recently for ‘investor relation services’… 300k shares for investor relations stuff at a company like Butler? Where do I sign?

So that’ll be something to watch.

Nonetheless, annualizing the recent quarter, Butler is trading at ~5.5x ev/ebitda for >25% ebitda growth. Talking to the company and watching the backlog I get the feeling that at least a few good quarters are ahead. Should these continue to show the same growth dynamic, I believe the shares still have plenty of room to go.

But this one needs to be watched more carefully. At the moment I think it’ll make for a good trade, though I’m not yet convinced it will be a good investment.

Unifiedpost (UPG Belgium - €115m market cap)

Unifiedpost is a niche SaaS player mainly operating within electronic invoicing, a market which is expected to have secular tailwinds due to regulatory tailwinds.

In simple terms, UPG helps business digitalize and streamline their financial and admin processes. The company provides cloud-based solutions to e.g. automate invoicing and payment processes, exchange documents digitally, ensure tax compliance across different countries, etc. UPG serves a few million customers worldwide over 30+ countries, mostly via longer-term contracts, providing a diversified and pretty visible revenue stream.

The company has been listed for roughly four years, and the shares have not exactly been a success. The share price hovered around €22 for some months after the IPO, but got crushed as rates rose and earnings disappointed.

Top-line growth has been flattish for the past few years paired with some heavy losses, the latter mainly the result of the company’s inability to generate operating leverage and big interest expenses on a pretty expensive – and large – debt position.

In short, UPG has been a total loser.

So, what makes this one worth looking into?

For starters, when I see a stock crap out and the share price remain flattish for some time despite whatever news the company puts out – I’m interested.

More importantly, it seems that UPG management has seen the light, and has recently embarked on a ‘let’s-get-to-cash-flow-positive-asap’ tour. The company announced a strategic review in April 2024, putting out some concrete, near-term goals of achieving a stable financial position and FCF break-even by 2025.

To do this, they have set three main goals:

Grow Core Digital Services: they aim to expand their higher-margin digital services business at a steady rate. This growth is essential because these services are more profitable compared to other parts of their business.

Control costs: keeping expenses in check is crucial to ensuring that the company can finally achieve some operating leverage.

Pay off debt: they have a significant and expensive debt burden to Francisco Partners. Paying this off will reduce its financial burden and drastically improve the balance sheet.

UPG wasted no time, and attacked the debt problem by selling some non-core businesses (given the targeted focus on their main digital services) at very decent prices. The largest asset sale has been the Wholesale Identity Access unit, which was sold for €133m (EV, incl. €7.7m earn-out), 16x FY23 ev/ebitda. This deal was finalised a month ago.

Not bad for a company with an EV of roughly €230m and €130m debt.

The proceeds from these divestments (which also include the sale of other smaller non-core businesses like Fitek/ONEA and 21 Grams) will push the company to a (small) net cash position, significantly improving the UPG’s cash generation profile.

Now there’s an actual path to becoming cash flow positive in the near-term. The company’s profile shifted strongly towards its digital activities which boast much higher gross margins (over 60%) compared to its legacy services (20-30%). Also, revenues from these activities should grow at >10% p.a. for the foreseeable future.

Given the shift in mix and return to growth, it’s not inconceivable for the company to get to mid-to-high single-digit ebitda this year. That would put it at 12-15x ev/ebitda on FY25e, with ebitda growing at 40-50% p.a. in the years thereafter as operating leverage kicks in.

But as always there’s some stuff to keep an eye on. While Digital Services revenues grew at a healthy rate over H1 24, Q3 showed a pretty large slowdown. There’s no Q3 call and I have yet to reach out to the company, but this is something to keep an eye on. It’s a small company, and its normal to have some hiccups, as long as they’re not structural.

But overall, here we have a company that went from being a indebted loser, to a growing company, with healthy gross margins and strong balance sheet – and the share price didn’t move.

The market’s clearly in wait-and-see mode, and that’s the opportunity.

If you value this write-up, please like and hit the “share” button below. Thank you.

IZEA looks like an interesting cigar-butt situation: Negative EV and Net Cash, I'm in!