ToffCap's Monday Monitor #19

ToffCap's Monday Monitor #19

Interesting event-driven trades and companies

ToffCap’s Monday Monitor provides a snapshot of interesting potential investments and event-driven trades we find while turning over many rocks, with a special focus on companies that screen cheaply and catalyst trades. The list is dynamic; it continues to grow and change. If you have interesting additions to the list, feel free to contact us at contact@toffcap.com or on Twitter.

Enjoy!

Disclaimer. ToffCap’s Monday Monitor is provided for informative purposes only. No due diligence has (yet) been performed on the names on this list. The list might change strongly on a regular basis. This overview does not constitute advice; always do your own due diligence.

Important notice. We would like to publish the TMM on a weekly basis, but we need a more critical mass. If you enjoy this service, please like and hit the “share” button below. Thank you.

Overview

I. Company watchlist

II. Catalyst trades

I. COMPANY WATCHLIST

Interesting companies with seemingly strong upside potential we have looked at recently.

Additions this week

Camellia (CAM UK – GBP 127m). We did not (yet) assess this idea, but @theotheraharon pitched this interesting set-up. Camellia is a marginally-profitable mostly-agricultural (tea and fruits) microconglomerate selling its stake in its insurance division for $100m, guiding to close in Q1 24. The company also started a process of winding-down its unprofitable UK fruits division. When a sale goes through, its net cash & marketable securities will approximate its market cap and far exceed its long-term obligations, which consist in large part of minor pension and deferred taxes. H/t @theotheraharon for the idea.

Paramount Global (PARA US – $9.8bn). We highlight this interesting recent write-up on from David Katunarić on Paramount Global. David makes an interesting (and humorous) case on the potential take-out (value) of the company. Byron Allen recently offered to take Paramount private for $14bn, which could accelerate interested parties to make a bid.

Befesa (BFSA Germany – EUR 1.3bn). Befesa faced quite a few headwinds over 2023, many of which should disappear and/or turn tailwinds over this year. Improved pricing will drive growth, and improving cost eficiencies (a.o. lower energy and treatment charges) will increasingly benefit margins. Synergy creation from the AZR acquisition should further help volume growth. Befesa is trading at ~11x 2024e ev/ebitda for (potentially) >20% ebitda growth over the next few years.

II. CATALYST TRADES

Event-driven trades and ideas.

New additions and updates

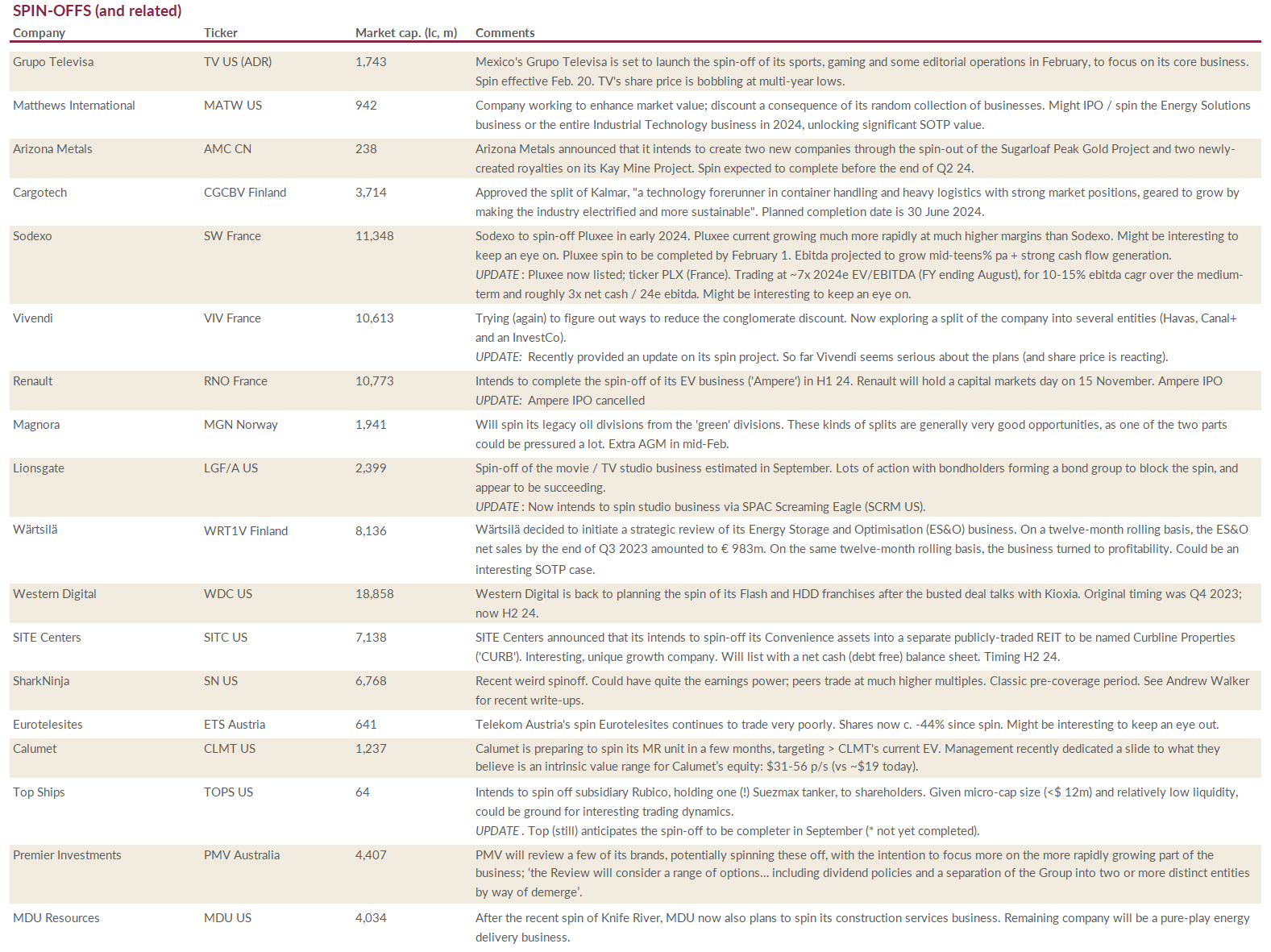

Grupo Televisa (TV US (ADR)). Mexico's Grupo Televisa is set to launch the spin-off of its sports, gaming and some editorial operations in February, to focus on its core business. Spin effective Feb. 20. TV's share price is bobbling at multi-year lows.

Sodexo (SW France). Sodexo to spin-off Pluxee in early 2024. Pluxee current growing much more rapidly at much higher margins than Sodexo. Might be interesting to keep an eye on. Pluxee spin to be completed by February 1. Ebitda projected to grow mid-teens% pa + strong cash flow generation.

UPDATE: Pluxee now listed; ticker PLX (France). Trading at ~7x 2024e EV/EBITDA (FY ending August), for 10-15% ebitda cagr over the medium-term and roughly 3x net cash / 24e ebitda. Might be interesting to keep an eye on.

Matthews International (MATW US). Company working to enhance market value; discount a consequence of its random collection of businesses. Might IPO / spin the Energy Solutions business or the entire Industrial Technology business in 2024, unlocking significant SOTP value.

Arizona Metals (AMC CN). Arizona Metals announced that it intends to create two new companies through the spin-out of the Sugarloaf Peak Gold Project and two newly-created royalties on its Kay Mine Project. Spin expected to complete before the end of Q2 24.

Vivendi (VIV France). Trying (again) to figure out ways to reduce the conglomerate discount. Now exploring a split of the company into several entities (Havas, Canal+ and an InvestCo).

UPDATE: Recently provided an update on its spin project. So far Vivendi seems serious about the plans (and share price is reacting).

Cargotech (CGCBV Finland). Approved the split of Kalmar, "a technology forerunner in container handling and heavy logistics with strong market positions, geared to grow by making the industry electrified and more sustainable". Planned completion date is 30 June 2024.

Renault (RNO France). Intends to complete the spin-off of its EV business ('Ampere') in H1 24. Renault will hold a capital markets day on 15 November. Ampere IPO targeted Q2 24, at EUR 8-10bn valuation.

UPDATE: Ampere IPO cancelled.

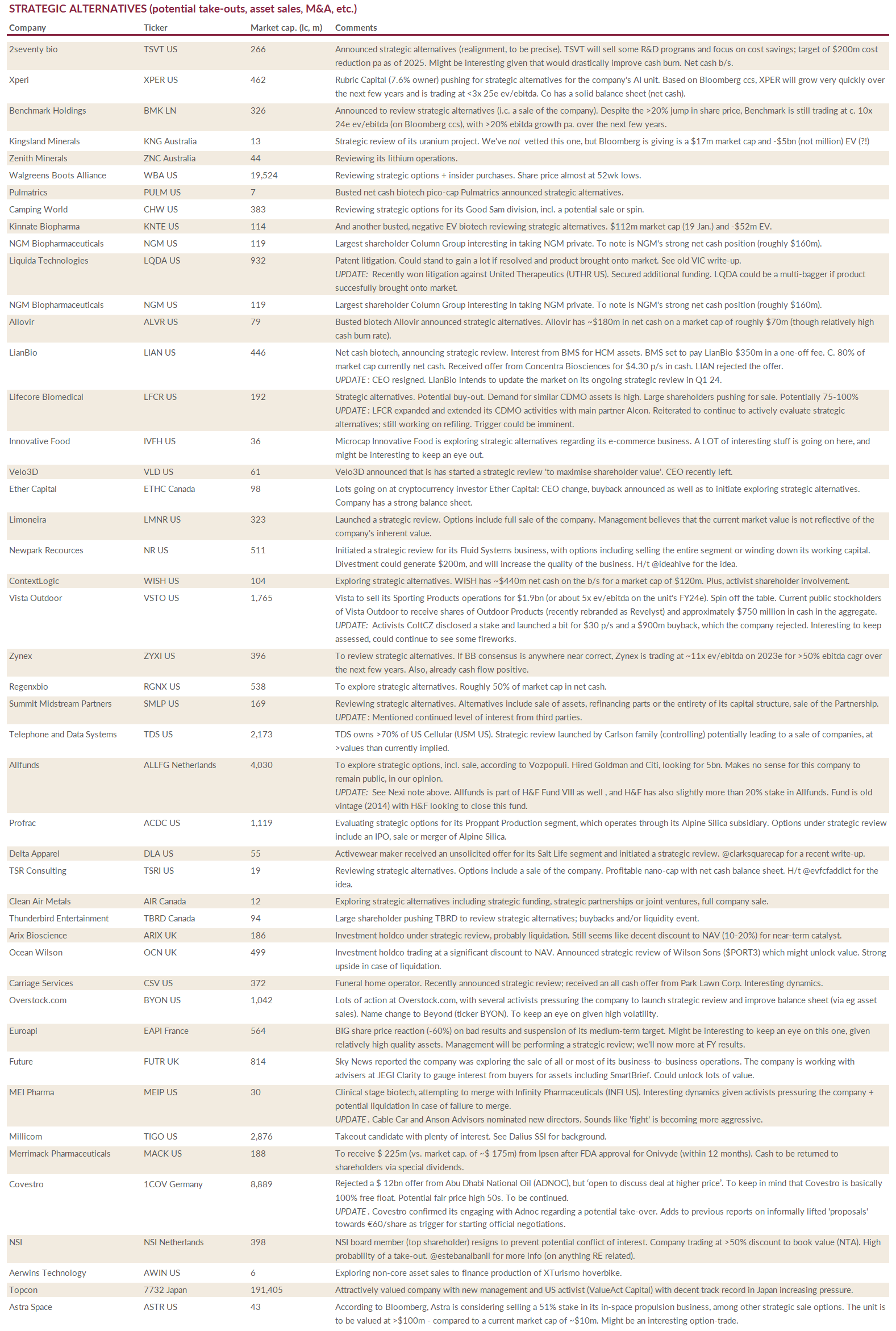

2seventy bio (TSVT US). Announced strategic alternatives (realignment, to be precise). TSVT will sell some R&D programs and focus on cost savings; target of $200m cost reduction pa as of 2025. Might be interesting given that would drastically improve cash burn. Net cash b/s.

Xperi (XPER US). Rubric Capital (7.6% owner) pushing for strategic alternatives for the company's AI unit. Based on Bloomberg ccs, XPER will grow very quickly over the next few years and is trading at <3x 25e ev/ebitda. Co. has a solid balance sheet (net cash).

Benchmark Holdings (BMK LN). Announced to review strategic alternatives (i.c. a sale of the company). Despite the >20% jump in share price, Benchmark is still trading at c. 10x 24e ev/ebitda (on Bloomberg ccs), with >20% ebitda growth pa. over the next few years.

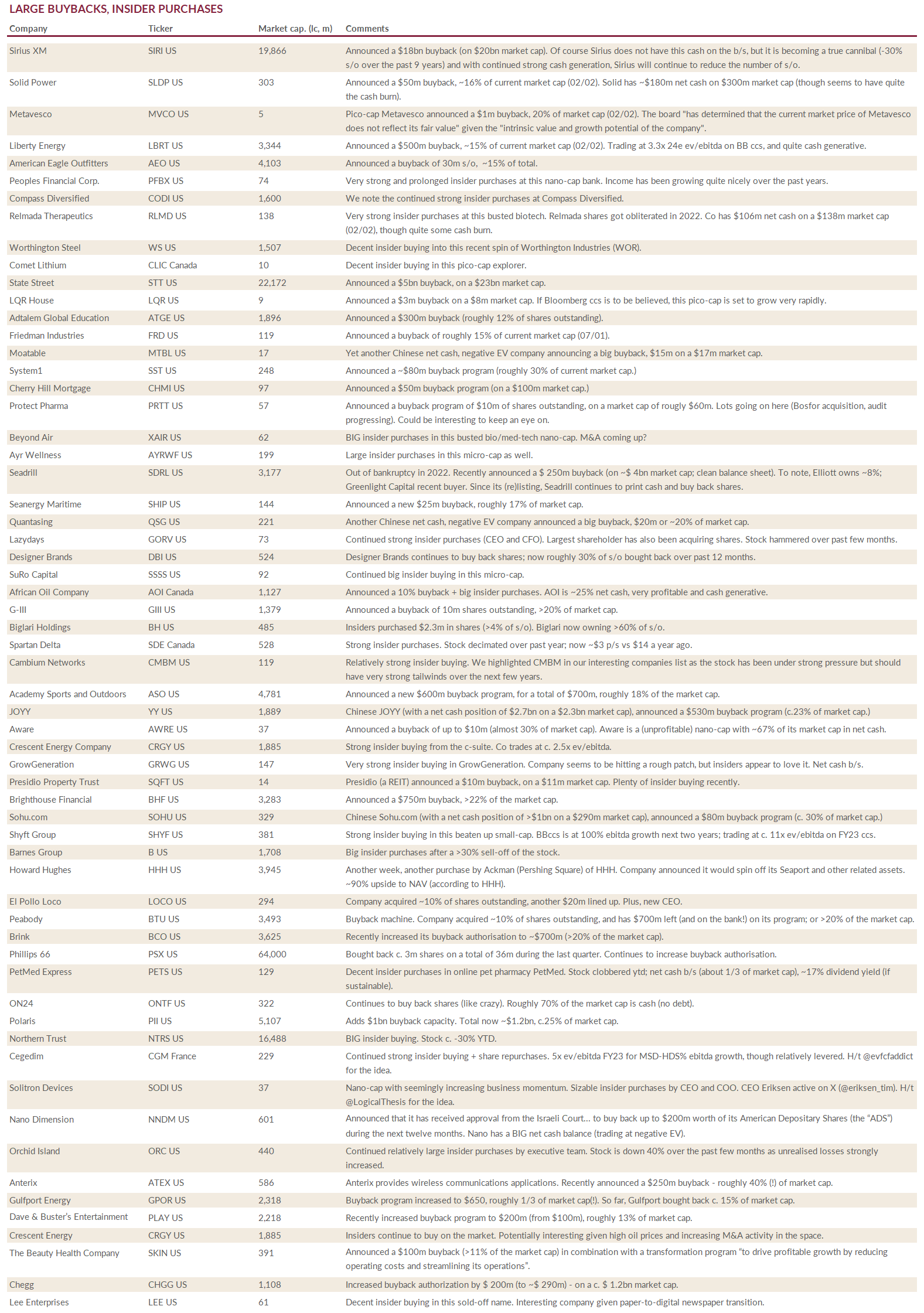

Sirius XM (SIRI US). Announced a $18bn buyback (on $20bn market cap). Of course Sirius does not have this cash on the b/s, but it is becoming a true cannibal (-30% s/o over the past 9 years) and with continued strong cash generation, Sirius will continue to reduce the number of s/o.

Solid Power (SLDP US). Announced a $50m buyback, ~16% of current market cap (02/02). Solid has ~$180m net cash on $300m market cap (though seems to have quite the cash burn).

Metavesco (MVCO US). Pico-cap Metavesco announced a $1m buyback, 20% of market cap (02/02). The board "has determined that the current market price of Metavesco does not reflect its fair value" given the "intrinsic value and growth potential of the company".

Liberty Energy (LBRT US). Announced a $500m buyback, ~15% of current market cap (02/02). Trading at 3.3x 24e ev/ebitda on BB ccs, and quite cash generative.

American Eagle Outfitters (AEO US). Announced a buyback of 30m s/o, ~15% of total.

Peoples Financial Corp (PFBX US). Very strong and prolonged insider purchases at this nano-cap bank. Income has been growing quite nicely over the past years.

Compass Diversified (CODI US). We note the continued strong insider purchases at Compass Diversified.

Relmada Therapeutics (RLMD US). Very strong insider purchases at this busted biotech. Relmada shares got obliterated in 2022. Co has $106m net cash on a $138m market cap (02/02), though quite some cash burn.

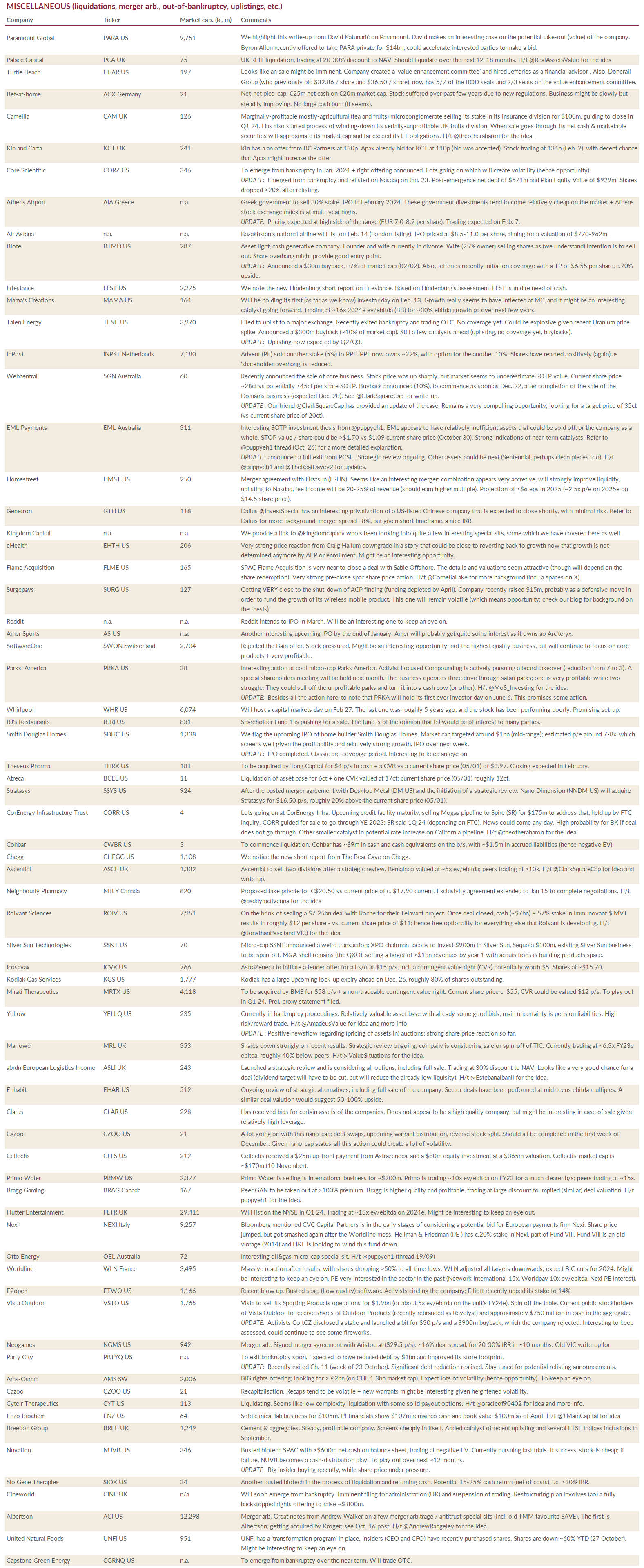

Paramount Global (PARA US). We highlight this write-up from David Katunarić on Paramount. David makes an interesting case on the potential take-out (value) of the company. Byron Allen recently offered to take PARA private for $14bn; could accelerate interested parties to make a bid.

Palace Capital (PCA UK). UK REIT liquidation, trading at 20-30% discount to NAV. Should liquidate over the next 12-18 months. H/t @RealAssetsValue for the idea.

Turtle Beach (HEAR US). Looks like an sale might be imminent. Company created a ‘value enhancement committee’ and hired Jefferies as a financial advisor . Also, Donerail Group (who previously bid $32.86 / share and $36.50 / share), now has 5/7 of the BOD seats and 2/3 seats on the value enhancement committee.

Bet-at-home (ACX Germany). Net-net pico-cap. €25m net cash on €20m market cap. Stock suffered over past few years due to new regulations. Business might be slowly but steadily improving. No large cash burn (it seems).

Camellia (CAM UK). Marginally-profitable mostly-agricultural (tea and fruits) microconglomerate selling its stake in its insurance division for $100m, guiding to close in Q1 24. Has also started process of winding-down its serially-unprofitable UK fruits division. When sale goes through, its net cash & marketable securities will approximate its market cap and far exceed its LT obligations. H/t @theotheraharon for the idea.

Kin and Carta (KCT UK). Kin has a an offer from BC Partners at 130p. Apax already bid for KCT at 110p (bid was accepted). Stock trading at 134p (Feb. 2), with decent chance that Apax might increase the offer.

Core Scientific (CORZ US). To emerge from bankruptcy in Jan. 2024 + right offering announced. Lots going on which will create volatility (hence opportunity).

UPDATE: Emerged from bankruptcy and relisted on Nasdaq on Jan. 23. Post-emergence net debt of $571m and Plan Equity Value of $929m. Shares dropped >20% after relisting.

Athens Airport (AIA Greece). Greek government to sell 30% stake. IPO in February 2024. These government divestments tend to come relatively cheap on the market + Athens stock exchange index is at multi-year highs.

UPDATE: Pricing expected at high side of the range (EUR 7.0-8.2 per share). Trading expected on Feb. 7.

Air Astana (n.a.). Kazakhstan's national airline will list on Feb. 14 (London listing). IPO priced at $8.5-11.0 per share, aiming for a valuation of $770-962m.

Talen Energy (TLNE US). Filed to uplist to a major exchange. Recently exited bankruptcy and trading OTC. No coverage yet. Could be explosive given recent Uranium price spike. Announced a $300m buyback (~10% of market cap). Still a few catalysts ahead (uplisting, no coverage yet, buybacks).

UPDATE: Uplisting now expected by Q2.

Biote (BTMD US). Asset light, cash generative company. Founder and wife currently in divorce. Wife (25% owner) selling shares as (we understand) intention is to sell out. Share overhang might provide good entry point.

UPDATE: Announced a $30m buyback, ~7% of market cap (02/02). Also, Jefferies recently initiation coverage with a TP of $6.55 per share, c.70% upside.

Lifestance (LFST US). We note the new Hindenburg short report on Lifestance. Based on Hindenburg's assessment, LFST is in dire need of cash.

Mama's Creations (MAMA US). Will be holding its first (as far as we know) investor day on Feb. 13. Growth really seems to have inflected at MC, and it might be an interesting catalyst going forward. Trading at ~16x 2024e ev/ebitda (BB) for ~30% ebitda growth pa over next few years.

Overview of ongoing event-driven trades

If you enjoy this service, please like and hit the “share” button below. Thank you.

Love it. The TMM continues to get better…

If you like Lifestance, you might want to take a look at Limes Schlosskliniken (Germany, private clinics for stress-related illnesses, mental and psychological disorders). Trading at <10x EBITDA Mult (EBITDA FY24 EURm 9,7 which includes 1.7m in ramp up costs for a new clinic); EV EURm 90) , FY23 headwinds disappearing (H1 was weak as cost increases could only be passed on with with some time lag) and back on track for their FY26 target (doubling revenue and EBITDA without new acquisition)