ToffCap's Monday Monitor #18

ToffCap's Monday Monitor #18

Interesting event-driven trades and companies

ToffCap’s Monday Monitor provides a snapshot of interesting potential investments and event-driven trades we find while turning over many rocks, with a special focus on companies that screen cheaply and catalyst trades. The list is dynamic; it continues to grow and change. If you have interesting additions to the list, feel free to contact us at contact@toffcap.com or on Twitter.

Enjoy!

Disclaimer. ToffCap’s Monday Monitor is provided for informative purposes only. No due diligence has (yet) been performed on the names on this list. The list might change strongly on a regular basis. This overview does not constitute advice; always do your own due diligence.

Important notice. We would like to publish the TMM on a weekly basis, but we need a more critical mass. If you enjoy this service, please like and hit the “share” button below. Thank you.

Overview

I. Company watchlist

II. Catalyst trades

I. COMPANY WATCHLIST

Interesting companies with seemingly strong upside potential we have looked at recently.

Additions this week

Pinetree Capital (PNP Canada – CAD 39m). If you like Constellation Software (CSU Canada) you might appreciate Pinetree Capital. Pinetree is a very small (and illiquid) listed closed-end with a focus on investing in value public software companies. The fund is very much tied to the Leonard family of Constellation; Damien Leonard (son of Mark Leonard, CEO and controlling owner of Constellation), is very much involved and owns c.35% of Pinetree. Other (formed) CSU executives are owners and operators as well. Though hard to calculate, the fund seems to be trading at ~10% discount to NAV, with NAV growing quite nicely. This might be an interesting opportunity to get into a micro-CSU at an early stage.

Celebrus Technology (CLBS UK – GBP 96m). Celebrus is an IT company that focusses on enterprise platforms for the collection, integration and analysis of customer data from a large variety of sources, for the purpose of a.o. data management, fraud assessment and regulatory analytics. The company has three product groups, but operates the business as a single business under the Celebrus product brand. The product which include 3rd Party, generated about 30% of sales while its Own IP generated some 25%. Support and Maintenance generated about 30% and the rest were generated from the Delivery Services. Celebrus is transitioning to an ARR model, targeting 75% of revenues, and is shifting from a partner-led to a direct sales model. 2024 has been a good year so for (FY ending March 2024), with ~50% top-line growth expected for the year. Growth is expected to continue strongly. The basic thesis is that this small net cash, cash-flow generating company will continue to grow the top-line and achieve operating leverage, leading to strong earnings growth. The combination of growth, discovery, improving liquidity, etc. will lead to an improved valuation.

Lassila & Tikanoja (LAT1V Finland – € 382m). L&T is a Finnish waste management and recycle services trading at a discount to (European) peers. The share price has been under pressure due to several temporary issues and a lack of guidance. L&T seems to have a strong strong competitive position, with >50% of revenues from the Circular Economy business (>80% of earnings). As the company continues to generate earnings and communication improves, there’s a good chance for L&T to rerate towards peer multiples (roughly 50-80% upside). There could also be a near-term catalyst from a potential disposals of the low-margin Facility Services businesses. Lastly, the company seems a good buyout candidate (to note that PE loves this sector).

SFC Energy (F3C Germany – € 330m). SFC Energy develops, produces and markets fuel cells for e.g. electric vehicles, remote industrial applications and mobile and stationary defense applications. This is an interesting high-growth and profitable play on the recurring sustainability theme. The order backlog growing nicely (roughly 40% yoy). The share prices suffered given strong selling pressure throughout the renewable equipment sector and poor performance of peers such as Plug Power. Near-term cost headwinds due to India factory ramp up. Might need to raise cash given limited free cash flow generation. Market cap + liquidity reaching interesting thresholds. Continued execution (ex capital raises) should rerate the name at some point. SFC is trading at ~20x FY23 ebitda, for >40% ebitda growth pa (BB est.) over the medium-term.

II. CATALYST TRADES

Event-driven trades and ideas.

New additions and updates

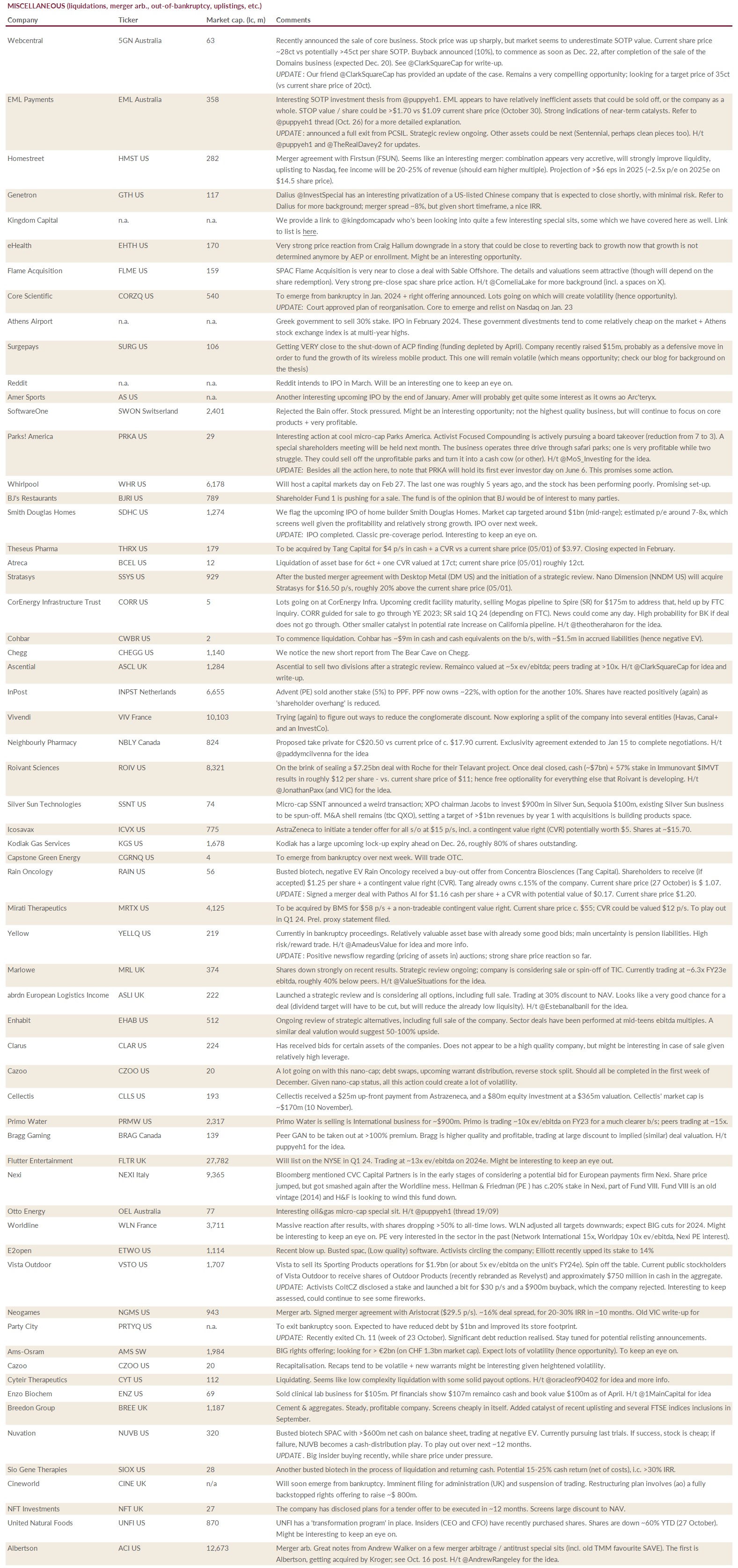

Webcentral (5GN Australia). Now 5G Networks. Recently announced the sale of core business. Stock price was up sharply, but market seems to underestimate SOTP value. Current share price ~28ct vs potentially >45ct per share SOTP. Buyback announced (10%), to commence as soon as Dec. 22, after completion of the sale of the Domains business (expected Dec. 20).

UPDATE: Our friend @ClarkSquareCap has provided an update on the case. Remains a very compelling opportunity; looking for a target price of 35ct (vs current share price of 18.5ct).

EML Payments (EML Australia). Interesting SOTP investment thesis from @puppyeh1. EML appears to have relatively inefficient assets that could be sold off, or the company as a whole. STOP value / share could be >$1.70 vs $1.09 current share price (October 30). Strong indications of near-term catalysts. Refer to @puppyeh1 thread (Oct. 26) for a more detailed explanation.

UPDATE: announced a full exit from PCSIL. Strategic review ongoing. Other assets could be next (Sentennial, perhaps clean pieces too). H/t @puppyeh1 and @TheRealDavey2 for updates.

Homestreet (HMST US). Merger agreement with Firstsun (FSUN). Seems like an interesting merger: combination appears very accretive, will strongly improve liquidity, uplisting to Nasdaq, fee income will be 20-25% of revenue (should earn higher multiple). Projection of >$6 eps in 2025 (~2.5x p/e on 2025e on $14.5 share price).

Genetron (GTH US). Dalius @InvestSpecial has an interesting privatization of a US-listed Chinese company that is expected to close shortly, with minimal risk. Refer to Dalius for more background; merger spread ~8%, but given short timeframe, a nice IRR.

Kingdom Capital (not a company). We provide a link to @kingdomcapadv who's been looking into quite a few interesting special sits, some which we have covered here as well. Link to the list is here.

eHealth (EHTH US). Very strong price reaction from Craig Hallum downgrade in a story that could be close to reverting back to growth now that growth is not determined anymore by AEP or enrollment. Might be an interesting opportunity.

Flame Acquisition (FLME US). SPAC Flame Acquisition is very near to close a deal with Sable Offshore. The details and valuations seem attractive (though will depend on the share redemption). Very strong pre-close SPAC share price action. H/t @CorneliaLake for more background (incl. a spaces on X).

Sodexo (SW France). Sodexo to spin-off Pluxee in early 2024. Pluxee current growing much more rapidly at much higher margins than Sodexo. Might be interesting to keep an eye on. Pluxee spin to be completed by February 1. Sodexo will hold a Capital Markets Day where medium-term guidance will be provided.

UPDATE: Sodexo held a capital markets day with an update of its strategy and releasing medium-term targets. Ebitda projected to grow mid-teens% pa + strong cash flow generation. Might be interesting to keep an eye on.

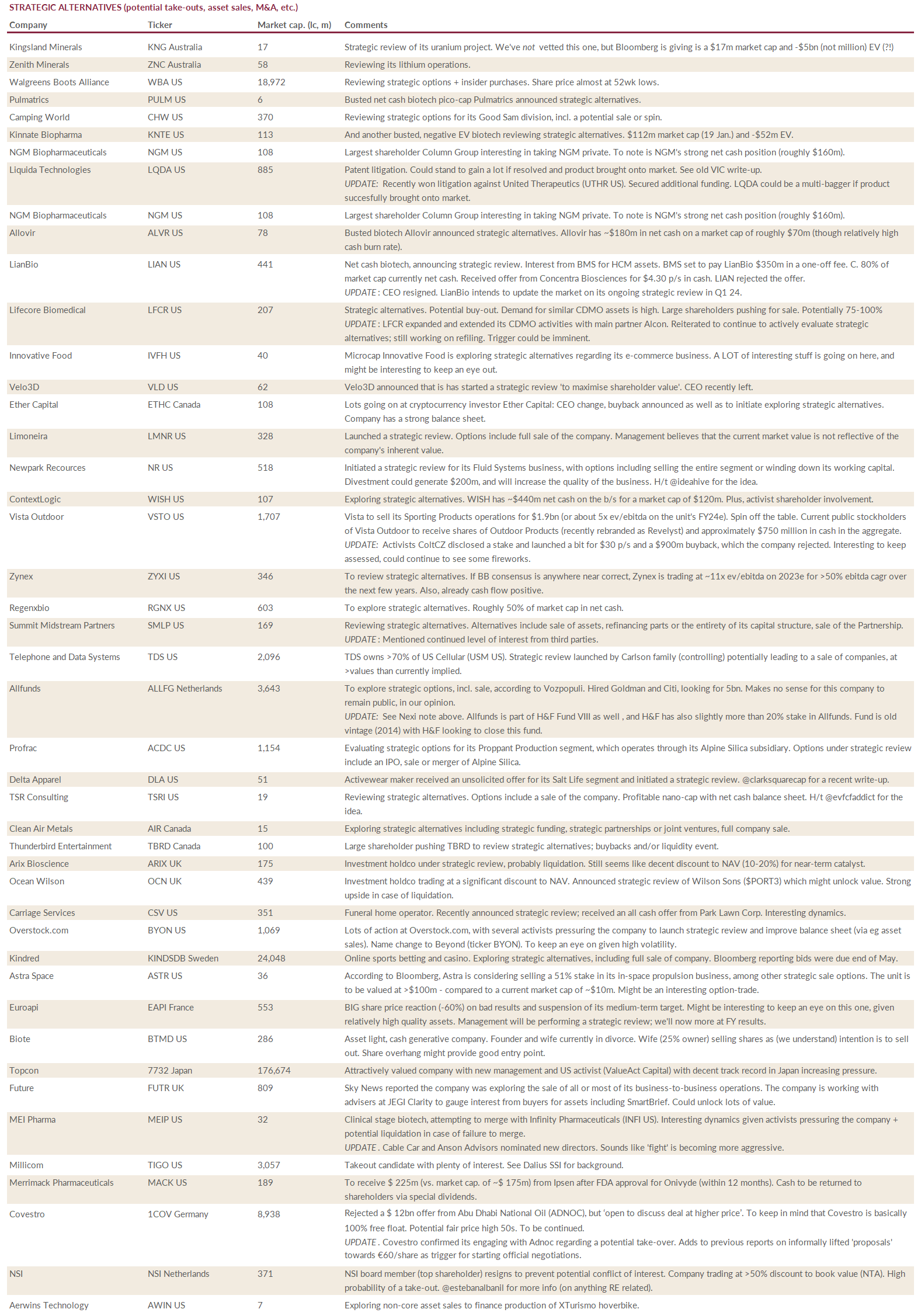

Walgreens Boots Alliance (WBA US). Reviewing strategic options + insider purchases. Share price almost at 52wk lows.

Core Scientific (CORZQ US). To emerge from bankruptcy in Jan. 2024 + right offering announced. Lots going on which will create volatility (hence opportunity).

UPDATE: Court approved plan of reorganization. Core to emerge and relist on Nasdaq on Jan. 23.

Athens Airport. Greek government to sell 30% stake. IPO in February 2024. These government divestments tend to come relatively cheap on the market + Athens stock exchange index is at multi-year highs.

Surgepays (SURG US). Getting VERY close to the shut-down of ACP finding (funding depleted by April). Company recently raised $15m, probably as a defensive move in order to fund the growth of its wireless mobile product. This one will remain volatile (which means opportunity; check our blog for background on the thesis)

Magnora (MGN Norway). Will spin its legacy oil divisions from the 'green' divisions. These kinds of splits are generally very good opportunities, as one of the two parts could be pressured a lot. Extra AGM in mid-Feb.

Worthington Steel (WS US). Decent insider buying into this recent spin of Worthington Industries (WOR).

Reddit. Reddit intends to IPO in March. Will be an interesting one to keep an eye on.

Amer Sports (AS US). Another interesting upcoming IPO by the end of January. Amer will probably get quite some interest as it owns a.o. Arc'teryx.

SoftwareOne (SWON Switzerland). Rejected the Bain offer. Stock pressured. Might be an interesting opportunity; not the highest quality business, but will continue to focus on core products + very profitable.

Pulmatrics (PULM US). Busted net cash biotech pico-cap Pulmatrics announced strategic alternatives.

Camping World (CHW US). Reviewing strategic options for its Good Sam division, incl. a potential sale or spin.

Kinnate Biopharma (KNTE US). And another busted, negative EV biotech reviewing strategic alternatives. $112m market cap (19 Jan.) and -$52m EV.

Comet Lithium (CLIC Canada). Decent insider buying in this pico-cap explorer.

State Street (STT US). Announced a $5bn buyback, on a $23bn market cap.

LQR House (LQR US). Announced a $3m buyback on a $8m market cap. If Bloomberg ccs is to be believed, this pico-cap is set to grow very rapidly.

Adtalem Global Education (ATGE US). Announced a $300m buyback (roughly 12% of shares outstanding).

Parks! America (PRKA US). Interesting action at cool micro-cap Parks America. Activist Focused Compounding is actively pursuing a board takeover (reduction from 7 to 3). A special shareholders meeting will be held next month. The business operates three drive through safari parks; one is very profitable while two struggle. They could sell off the unprofitable parks and turn it into a cash cow (or other). H/t @MoS_Investing for the idea.

UPDATE: Besides all the ongoing action here, to note that PRKA will hold its first ever investor day on June 6. This promises some action.

Whirlpool (WHR US). Will host a capital markets day on Feb 27. The last one was roughly 5 years ago, and the stock has been performing poorly. Promising set-up.

BJ's Restaurants (BJRI US). Shareholder Fund 1 (~5.6%) is pushing for a sale. The fund is of the opinion that BJ would be of interest to many parties.

Kingsland Minerals (KNG Australia). Strategic review of its uranium project. We've not assessed this one, but Bloomberg is giving is a $17m market cap and -$5bn (not million) EV (?!)

Zenith Minerals (ZNC Australia). Reviewing its lithium operations.

Smith Douglas Homes (SDHC US). We flag the upcoming IPO of home builder Smith Douglas Homes. Market cap targeted around $1bn (mid-range); estimated p/e around 7-8x, which screens well given the profitability and relatively strong growth. IPO over next week.

UPDATE: IPO completed. Classic pre-coverage period. Interesting to keep an eye on.

Overview of ongoing event-driven trades

SPIN-OFFS (and related)

STRATEGIC ALTERNATIVES, POTENTIAL TAKE-OUTS, ASSET SALES, M&A, etc.

LARGE BUYBACKS, INSIDER PURCHASES

MISCELLANEOUS (liquidations, merger arb., out-of-bankruptcy, uplistings, etc.)

If you enjoy this service, please like and hit the “share” button below. Thank you.

Thanks for doing these. Always interesting to see some cool new ideas.

Lassila & Tikanoja (LAT1V Finland – € 382m) seems interesting. Does anyone have any extra info on the "temporary issues" the company is/was going through?

I suppose we don't like that current EPS is still below 2015-2016 levels.

Have you looked at Capri?